: Age, Height, Family, Movies and TV Shows, Career, Net Worth and More")

For many UK small business owners, personal tax sits somewhere between “I’ll deal with it later” and “my accountant handles that”. The problem is that by the time tax is calculated, most of the important decisions have already been made. Salary has been set, dividends declared, pension contributions either paid or missed.

The Personal Allowance sits quietly underneath all of this. It rarely changes, rarely makes headlines, and yet it plays a decisive role in how much income you actually keep. In the 2025/26 tax year, that role is becoming more pronounced.

Personal Allowance 2025/26: the number everyone knows – and why it still catches people out

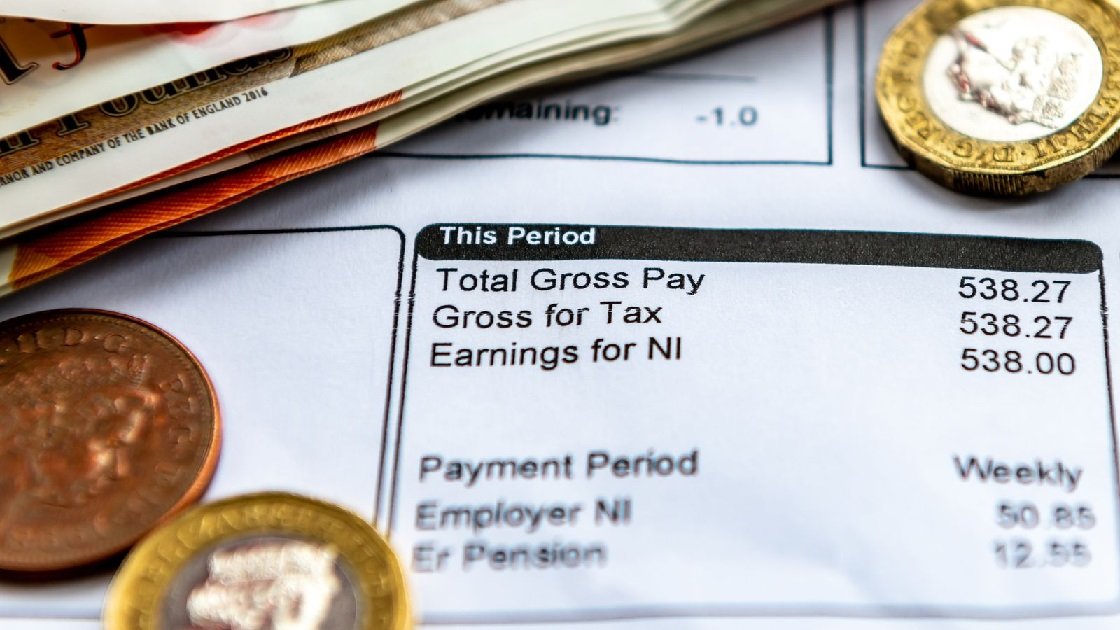

For the tax year running from 6 April 2025 to 5 April 2026, the standard UK Personal Allowance remains £12,570. In theory, that is the amount you can earn before income tax applies.

What often gets overlooked is that this figure has been frozen for several years. While salaries, dividends, and even interest on savings have risen, the tax-free threshold has not. As a result, many business owners are paying tax on income that would previously have sat comfortably within the allowance.

Another common misunderstanding is that the allowance applies neatly to one income source. It doesn’t. HMRC applies it across your total taxable income, which matters if you earn through a mix of salary, profits, dividends, or pensions.

Who actually qualifies for the Personal Allowance

For most people, entitlement is straightforward. If you are a UK tax resident, you are normally entitled to the Personal Allowance regardless of whether you are employed, self-employed, or running a limited company.

Where confusion often arises is around nationality and visa status. These are rarely decisive on their own. Some non-residents can still claim the allowance, particularly UK nationals living abroad or residents of countries with relevant double taxation agreements. In practice, tax residence and treaty rules matter far more than job title or immigration category.

The £100,000 threshold that quietly reshapes your tax bill

Once adjusted net income exceeds £100,000, the Personal Allowance starts to be withdrawn. This is where the system becomes far less intuitive.

For every £2 earned above £100,000, £1 of allowance is lost. By the time income reaches £125,140, the allowance disappears completely. This creates a narrow income band with an unusually high effective marginal tax rate, often close to 60%.

What’s important is that adjusted net income is not simply your headline earnings. It can be reduced through legitimate reliefs such as pension contributions and Gift Aid donations. For business owners hovering around the threshold, this often means the taper is not inevitable – but only if it’s addressed before the tax year ends.

A quick reality check at this stage can save a lot of regret later. Many people use a take home calculator to see how an extra dividend or bonus would interact with the taper before committing to it.

Why this matters in practice

The taper doesn’t just increase tax – it distorts incentives. Earning slightly more can leave you noticeably worse off unless reliefs are used deliberately.

How the Personal Allowance fits with UK income tax bands

The Personal Allowance is always applied before income tax bands come into play. Once it is used up, income is taxed according to the rates that apply in your part of the UK.

England and Northern Ireland follow the familiar basic, higher, and additional rate structure. Wales currently mirrors these rates. Scotland applies a different set of bands for non-savings income, but the Personal Allowance itself remains UK-wide.

RegionKey pointEngland & NIStandard UK rates applyScotlandDifferent bands, same Personal AllowanceWalesRates currently aligned with England

For business owners, the practical takeaway is that regional differences affect how income is taxed after the allowance, not whether the allowance applies.

Why your tax code deserves more attention

For anyone paid through PAYE – including directors on payroll and pensioners – the Personal Allowance is delivered via the tax code. The standard code for 2025/26 is 1257L, which reflects the full allowance.

Complications arise when income becomes fragmented. Multiple jobs, pensions, benefits in kind, or underpaid tax from previous years can all lead to codes where no allowance is applied to a particular income stream. Codes such as BR or 0T are common in these situations and can significantly reduce monthly take-home pay, even if the year-end position eventually balances out.

K codes are especially worth reviewing. They indicate that deductions exceed the allowance, often due to benefits in kind or earlier underpayments. While HMRC caps how much tax can be collected per pay period, a K code should always prompt a closer look.

How other allowances sit alongside the Personal Allowance

The Personal Allowance works alongside other reliefs rather than replacing them. Marriage Allowance allows a lower-earning spouse or civil partner to transfer part of their unused allowance. Savings income may benefit from the Personal Savings Allowance or the Starting Rate for Savings, but only after the Personal Allowance has already been used.

The Dividend Allowance, now £500 for 2025/26, is frequently misunderstood. Dividends within the allowance are taxed at 0%, but they still use up tax bands. For director-shareholders, this detail has a direct impact on how much dividend income is taxed at higher rates.

Which income uses the allowance first – and why it matters

HMRC applies the Personal Allowance in a fixed order. Non-savings income such as salary, trading profits, or pensions uses it first. Savings income comes next, with dividends last.

This ordering explains why two people with similar total income can face very different tax outcomes depending on how that income is structured.

Personal Allowance and National Insurance are not the same thing

One of the most persistent misconceptions is that the Personal Allowance also applies to National Insurance. It does not.

National Insurance has its own thresholds and rules, which vary for employees, the self-employed, and directors. It is entirely possible to pay NI while paying no income tax, or the other way around.

Making the allowance work in real life

For most small business owners, optimising the Personal Allowance is not about aggressive planning. It is about structure, timing, and visibility.

That might mean setting director salary close to the allowance, reviewing dividend timing, or using pension contributions more deliberately. It also means having a clear view of income and obligations throughout the year, rather than discovering issues at filing time.

Tools like ANNA Money support this approach by keeping income, expenses, and tax obligations visible in one place, making it easier to plan ahead rather than correct mistakes retrospectively.

A simple director-shareholder example

Take a director paying themselves a salary of £12,570 and dividends on top. The salary is covered by the Personal Allowance. Dividends then benefit from the dividend allowance, with the remainder taxed at dividend rates.

This structure remains common not because it is clever, but because it aligns naturally with how the allowance and tax bands are designed – provided it is reviewed regularly.

Final thoughts

The Personal Allowance may look static, but its impact is not. As thresholds remain frozen and incomes rise, it plays a growing role in determining how much you actually keep.

For small business owners, understanding how it works in 2025/26 – and revisiting it as circumstances change – is one of the simplest, most compliant ways to protect take-home pay.

Refresh Date: April 9, 2026